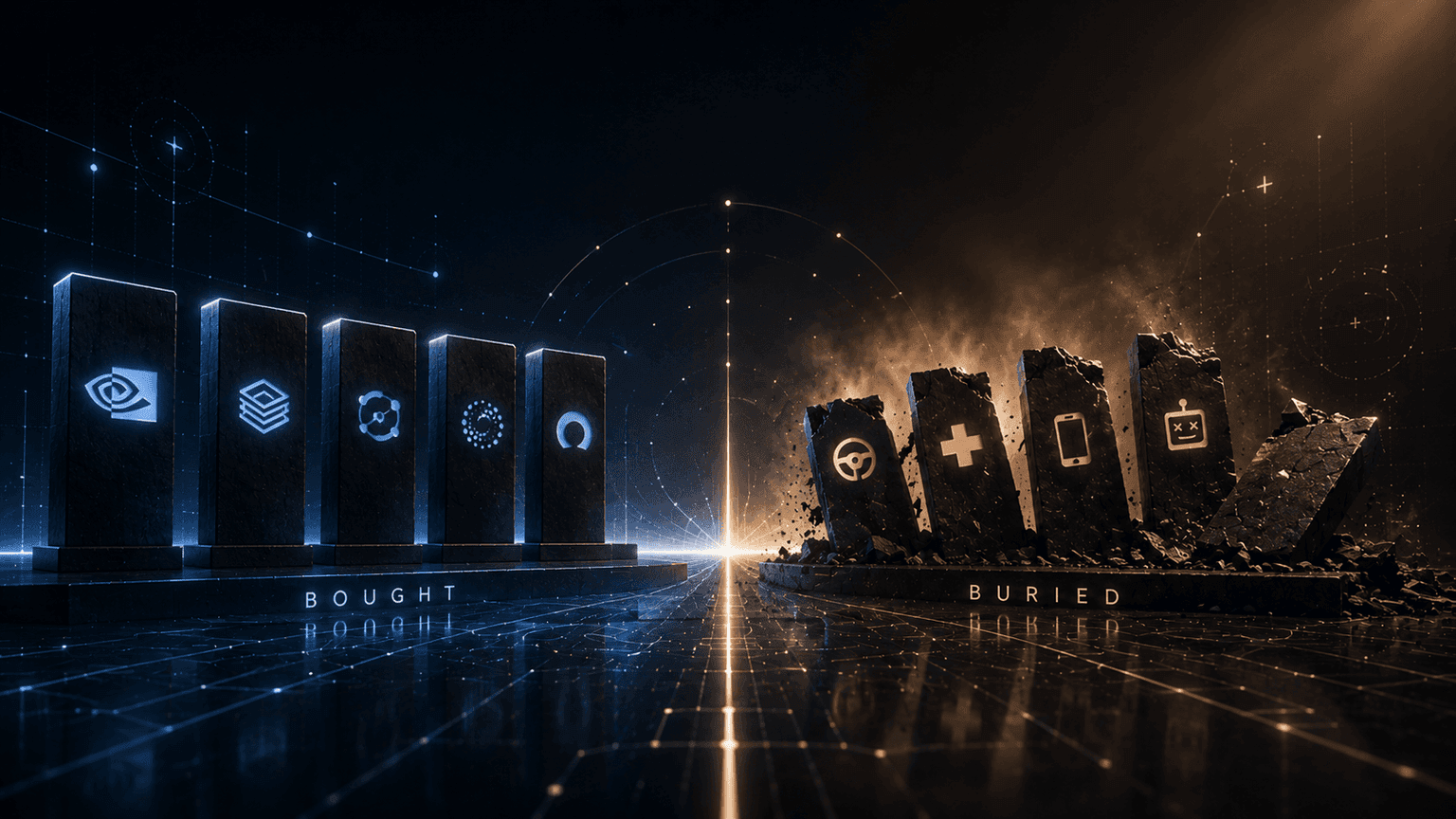

Bought or buried: inside the 2026 AI consolidation

The AI startup boom is over, and in 2026 the survivors are sorting into two piles: bought and buried. On one side, an AI acquisition wave — NVIDIA, Databricks, Meta, and a line of software incumbents are quietly buying up the AI stack, startup by startup. On the other, the overpromisers are collapsing outright. The AI consolidation of 2026 isn't a single dramatic crash; it's a steady sorting of which companies were building something worth owning and which were selling a story. This is a look at who got acquired, who didn't make it, and what the pattern says about where AI value is actually accruing.

For the full roster of shutdowns and acquisitions we track, our AI graveyard is the running record, and our earlier piece on the AI tools that died or got acquired catalogs the casualties. This post is the read on top of that data: not a list, but the shape of the consolidation.

Update, August 2, 2026: the courtroom became the loudest consolidation channel

July did not produce a deal bigger than the SpaceX-Cursor record below. It produced something more consequential for anyone building on these tools: two rulings that put a price on the training data underneath them.

A US court approved the largest copyright settlement in the country's history. On July 20, Judge Araceli Martínez-Olguín signed off on Anthropic's $1.5 billion settlement with book authors over pirated copies used in training — roughly $3,000 per book across more than 482,000 works, about 91% of which have been claimed. Eleven days later, on July 31, the Munich Regional Court ruled in GEMA v. Suno that training a music model on protected compositions, and generating outputs from them, infringes German copyright — the first decision anywhere to say AI training needs a license rather than falling under a text-and-data-mining exception. Suno is weighing an appeal.

Read together with the label settlements we covered in the July update, that is the same consolidation story arriving through a different door. Rights holders are not buying AI companies; they are establishing a toll. The effect on the market is identical to an acquisition wave — it raises the cost of being an independent model company, and it advantages the players who can write the check.

Robin AI is what "bought or buried" looks like when both happen at once. The legal-AI startup's planned funding round collapsed in late 2025; its managed-services arm was sold off, its technology and engineering team were hired into Microsoft to build legal features inside Word, and the company itself went into a winding-up process. No headline acquisition, no shutdown notice — the parts were worth more than the whole, and the brand simply stopped existing. Our registry carries it as acquired-and-sunset rather than acquired-and-operating, which is the distinction this piece exists to make. Expect more of this shape: 2026's mid-tier AI companies are being disassembled more often than they are being bought.

The registry numbers, refreshed. As of August 2, 2026 our AI graveyard tracks 219 AI tools that shut down or were acquired — 101 gone entirely, 55 acquired and sunset, and 63 acquired but still shipping under their own brand. That is up from 193 on July 8: twenty-six additions in under a month, and the fastest stretch of registry growth since we started keeping it. The month's full ledger, including the deals and shutdowns that didn't change the thesis, is in our July 2026 news roundup.

Update, July 12, 2026: the consolidation reached the application layer

When we first published this piece in early June, the pattern was infrastructure giants buying the stack and incumbents bolting on. A month later the consolidation jumped a layer — and set a record doing it.

SpaceX acquired Cursor and its parent Anysphere in a deal reported at $60 billion — the largest startup acquisition ever recorded. Whatever the strategic logic (talent, tooling, and a software arm for an interplanetary industrial base is the stated frame), the signal is unmistakable: application-layer AI companies with real revenue are no longer just consolidators' targets at the margins; they are the biggest prizes in tech. The footnote that makes it a parable: two days after the SpaceX deal was announced, Cursor closed an acquisition of its own — Continue, one of the earliest open-source coding agents. In the 2026 market, the food chain moves fast enough that a company can be buying and being bought in the same week.

The rest of the summer's deals confirm the two original patterns still running underneath. On the chip-adjacent layer, Qualcomm bought the AI-infrastructure startup Modular for a reported $4 billion — the same keep-the-optimization-layer-close logic as NVIDIA's inference buys. On the bolt-on side, Salesforce bought Intercom's Fin in a deal reported around $3.6 billion — months after closing its purchase of the AI pipeline platform Qualified — and June closed with a cluster of them: Adobe took the image-enhancement suite Topaz Labs, Superhuman absorbed the AI detector GPTZero, and Schneider Electric paid $3.1 billion for the industrial-data platform Cognite. From our registry's June and July additions: Zoom picked up the community-intelligence platform Common Room, HubSpot bought the signal-based sales tool Warmly, and Livestorm absorbed Qlip. All are running as acquired-but-operating brands for now; our AI graveyard tracks that state explicitly, because history says post-close sunsets tend to arrive within the year.

One more consolidation channel opened that isn't an acquisition at all: the courtroom. Universal's settlement with Udio and Warner's with Suno converted copyright lawsuits into licensing deals and a joint platform — the labels effectively buying control of AI music's distribution without buying the companies. Our AI music generators review covers what that means for users.

And the capital backdrop makes the sorting sharper, not gentler: roughly 80% of Q2 venture investment went to AI startups, part of a record $392 billion North American first half. The consolidation of 2026 is not happening because money ran out. It's happening because buyers and markets have decided which AI businesses are worth owning — and are paying record prices for those, while the rest get nothing.

The shape of the 2026 AI consolidation

Two forces are running at once. The first is vertical integration: the companies that own the expensive layers of AI — chips, data infrastructure, model training — are buying the smaller companies that optimize, serve, and feed those layers. The second is bolt-on: software incumbents that missed the first AI wave are buying their way into it, acquiring a vertical AI product rather than building one.

What ties the two together is that the acquired companies almost all sold something concrete — an inference optimizer, a feature store, a legal-research engine, a data-enrichment layer. The companies that died, by contrast, mostly sold a promise: full self-driving, AI that runs your clinic, an app built "by AI" with no engineers. The market in 2026 is paying for picks and shovels and burying the gold-rush stories.

NVIDIA is buying the inference layer

The most active acquirer in the AI stack isn't a hyperscaler buying models — it's NVIDIA buying the layer that makes models cheaper to run. Across 2024 and 2025, NVIDIA absorbed a string of inference- and model-optimization startups: Lepton AI, OctoAI (the former OctoML), and Deci, followed in mid-2025 by CentML — a Toronto startup whose software sits between AI models and the chips that run them, in a deal reportedly worth up to $400M.

The logic is consistent. NVIDIA already sells the chips; owning the companies that squeeze more tokens-per-second out of those chips deepens the moat and keeps the optimization expertise in-house rather than helping rival silicon. Each of these startups had raised real venture money to build genuinely useful technology — and each concluded that the better outcome was to join the company that defines the hardware they optimize for. When the most valuable company on earth is acqui-hiring your whole category, that tells you where the category's ceiling is.

Databricks and the data-layer land grab

Databricks ran the same playbook one layer up, on data and training. Its $1.3B acquisition of MosaicML in 2023 set the template — buy the model-training infrastructure, fold it into the platform — and in 2025 it kept going, acquiring the real-time feature store Tecton (built by the team behind Uber's machine-learning platform, reportedly valued around $900M) to round out the data layer that feeds AI agents.

The pattern across NVIDIA and Databricks is the tell of the 2026 consolidation: the infrastructure giants are assembling the full AI stack by acquisition, because the parts are now cheaper to buy than to wait out. For startups in those layers, "independent forever" stopped being the plan.

The incumbents bolting on AI

The second wave of buyers is software incumbents adding AI to suites that were starting to look dated. These deals are less about owning infrastructure and more about not getting left behind:

- Thomson Reuters bought Casetext for roughly $650M, and its CoCounsel AI assistant became the centerpiece of Thomson Reuters' legal-AI push.

- ServiceNow acquired Moveworks in a deal reported around $2.85B — its largest ever — to bolt an enterprise AI copilot onto the ServiceNow platform.

- Salesloft absorbed Drift, folding conversational marketing into its sales-engagement stack.

- Palo Alto Networks, Cisco, and IBM each bought into AI security and data — Protect AI, Robust Intelligence, and DataStax respectively — adding AI-native capabilities to security and data portfolios.

- MongoDB bought Voyage AI for its embedding models; Adobe took Rephrase.ai; Google picked up the text-to-UI startup Galileo AI.

None of these are category-defining bets the way the NVIDIA deals are. They're the sound of incumbents deciding it's cheaper to buy a working AI product than to build one and hope.

The soft landings: acqui-hires and fire-sales

Not every acquisition is a win. A third category is the soft landing — a sale that's really a rescue, where the product mattered less than the team or the patents.

The clearest example is Humane, whose AI Pin was one of the most-hyped hardware launches of the decade and one of its fastest flops. HP acquired Humane's assets for around $116M in early 2025 and discontinued the Pin almost immediately — buying the talent and IP, not the product. Meta, meanwhile, picked up Limitless in December 2025 — the AI-pendant company formerly known as Rewind — folding its team into Meta's AI-wearables push and winding the pendant down. It's the kind of personal-AI acqui-hire that has become a standard exit for promising teams that couldn't find a standalone market.

A soft landing still beats the alternative — which a lot of 2026's most famous names didn't get.

The buried: who didn't get bought

The companies that died in 2026's shakeout share a trait: they were too capital-hungry, too far from revenue, or too dependent on a promise that didn't hold — and so no acquirer wanted them at any price.

The starkest is Builder.ai, the Microsoft-backed "build an app with AI" startup that raised over $450M and was once valued north of a billion. It collapsed into insolvency in 2025 amid reporting that its "AI" leaned heavily on human engineers and that its revenue had been overstated — a near-perfect parable for the gap between AI marketing and AI substance.

The other casualties cluster around the most capital-intensive AI promises:

- Autonomous driving buried the most money. Cruise — into which GM had poured well over $10B — was wound down as a robotaxi business in late 2024. Argo AI, backed by Ford and Volkswagen, shut down in 2022, and Embark Trucks followed in the autonomous-trucking wind-down.

- AI healthcare buried the rest. Olive AI, once valued around $4B, wound down in 2023 and sold off its parts. Forward, the primary-care startup that raised roughly $650M to build AI-run "CarePods," shut down in late 2024. Babylon Health, which went public via SPAC at a multibillion-dollar valuation, collapsed in 2023.

For the complete list, the AI graveyard is the running tally. The throughline is that none of these died for lack of ambition. They died because the thing they promised — a car that drives itself, a clinic that runs itself, an app that builds itself — turned out to cost far more, and work far less, than the pitch deck said.

What the consolidation actually tells you

Read together, the bought and the buried point at the same conclusion, and it's the same one our look at the AI capex bubble reached from the spending side: in 2026, durable AI value is accruing to the infrastructure and to focused, revenue-generating products — not to the moonshots.

The acquirers are telling you what they think is worth owning: the layer that makes models efficient (NVIDIA), the data and training stack (Databricks), and working vertical products with real customers (the incumbents). The graveyard is telling you what isn't: anything that needed billions and years to maybe work. If you're evaluating an AI tool in 2026, that's the lens — is this a pick-and-shovel business with revenue, or a gold-rush story burning capital toward a promise? The market has started answering that question for everyone, one acquisition and one shutdown at a time.

Frequently asked questions

Has any court ruled on whether AI training is legal? Yes, as of July 2026. A US court approved Anthropic's $1.5 billion settlement with book authors on July 20 — the largest copyright settlement in US history, though a settlement rather than a merits ruling — and on July 31 the Munich Regional Court held in GEMA v. Suno that training a music model on protected works infringes German copyright. The US fair-use question itself remains open: Sony's case against Suno has dispositive motions due April 2027.

Who is buying AI startups in 2026? Two groups. Infrastructure giants — chiefly NVIDIA (buying inference and model-optimization startups like Lepton AI, OctoAI, and Deci) and Databricks (buying data and training infrastructure like MosaicML and Tecton) — are vertically integrating the AI stack. Software incumbents — Thomson Reuters, ServiceNow, Salesloft, Palo Alto Networks, Cisco, IBM, Adobe, and others — are bolting AI products onto existing suites.

Why is NVIDIA acquiring so many AI companies? NVIDIA already sells the chips that run AI models; buying the startups that optimize inference and model performance deepens its moat, keeps that expertise in-house, and makes its hardware more valuable. Owning the optimization layer is cheaper and faster than letting it develop independently — possibly to the benefit of rival chipmakers.

What happened to Builder.ai? Builder.ai, a Microsoft-backed startup that promised AI-built software and raised over $450M, collapsed into insolvency in 2025 amid reporting that its "AI" depended heavily on human engineers and that its revenue had been overstated. It became the year's emblematic case of AI marketing outrunning AI substance.

What were the biggest AI acquisitions of 2026? The record-setter is SpaceX's reported $60B acquisition of Cursor and its parent Anysphere in Q2 2026 — the largest startup acquisition ever. Behind it: Qualcomm's reported $4B purchase of Modular, Salesforce's roughly $3.6B deal for Intercom's Fin, Schneider Electric's $3.1B purchase of Cognite, ServiceNow's roughly $2.85B purchase of Moveworks, NVIDIA's string of inference-startup buys (Lepton AI, OctoAI, Deci, CentML), and Thomson Reuters' ~$650M Casetext acquisition. Terms for many deals weren't disclosed.

Which AI tools were acquired in June and July 2026? From our registry: Cursor (with its own June acquisition, Continue) went to SpaceX, Modular to Qualcomm, Topaz Labs to Adobe, GPTZero to Superhuman, Cognite to Schneider Electric, Intercom's Fin to Salesforce, Common Room to Zoom, Warmly to HubSpot, and Qlip to Livestorm. Most are running as acquired-but-still-operating brands, a state our AI graveyard tracks separately from shutdowns.

Is the AI bubble bursting? Not exactly bursting — sorting. The 2026 consolidation is separating durable AI businesses (infrastructure and revenue-generating products, which get bought) from capital-intensive promises (autonomous driving, AI healthcare moonshots, and "AI" that was really humans, which get buried). It's a maturation of the market more than a crash.

Where to go next

For the full record of what's shut down and what's been acquired, our AI graveyard is the running tally, and our AI tools that died or got acquired piece catalogs the casualties in depth. For the spending side of the same story, our AI capex bubble analysis looks at where the AI money is — and isn't — coming back.

The pattern worth remembering as the shakeout continues: in 2026, the AI market is buying picks and shovels and burying promises. Position accordingly.

— The ToolDirectory.AI editorial team

Get the weekly roundup.

One email each Friday. The week's additions, the week's deaths, and one thing we changed our mind about. No drip sequences, no AI-generated filler.